Diverse Outlook

Diverse Outlook

The mining industry has faced falling prices as supply chains have adjusted to interruptions from covid-19 and Russia’s invasion of Ukraine. Even so, prices remain generally elevated versus the 20-year average as well as relative to cost support.

After many years of generally focusing on returning excess cash to shareholders, elevated commodities prices are now encouraging the miners to once again tilt to growth through new developments, expansions, and mergers and acquisitions. This is particularly the case in energy transition commodities.

This industry searches for, develops, extracts, and processes commodities including iron ore, metallurgical coal, copper, and gold, and ships them to customers, often in an intermediate form, such as a concentrate.

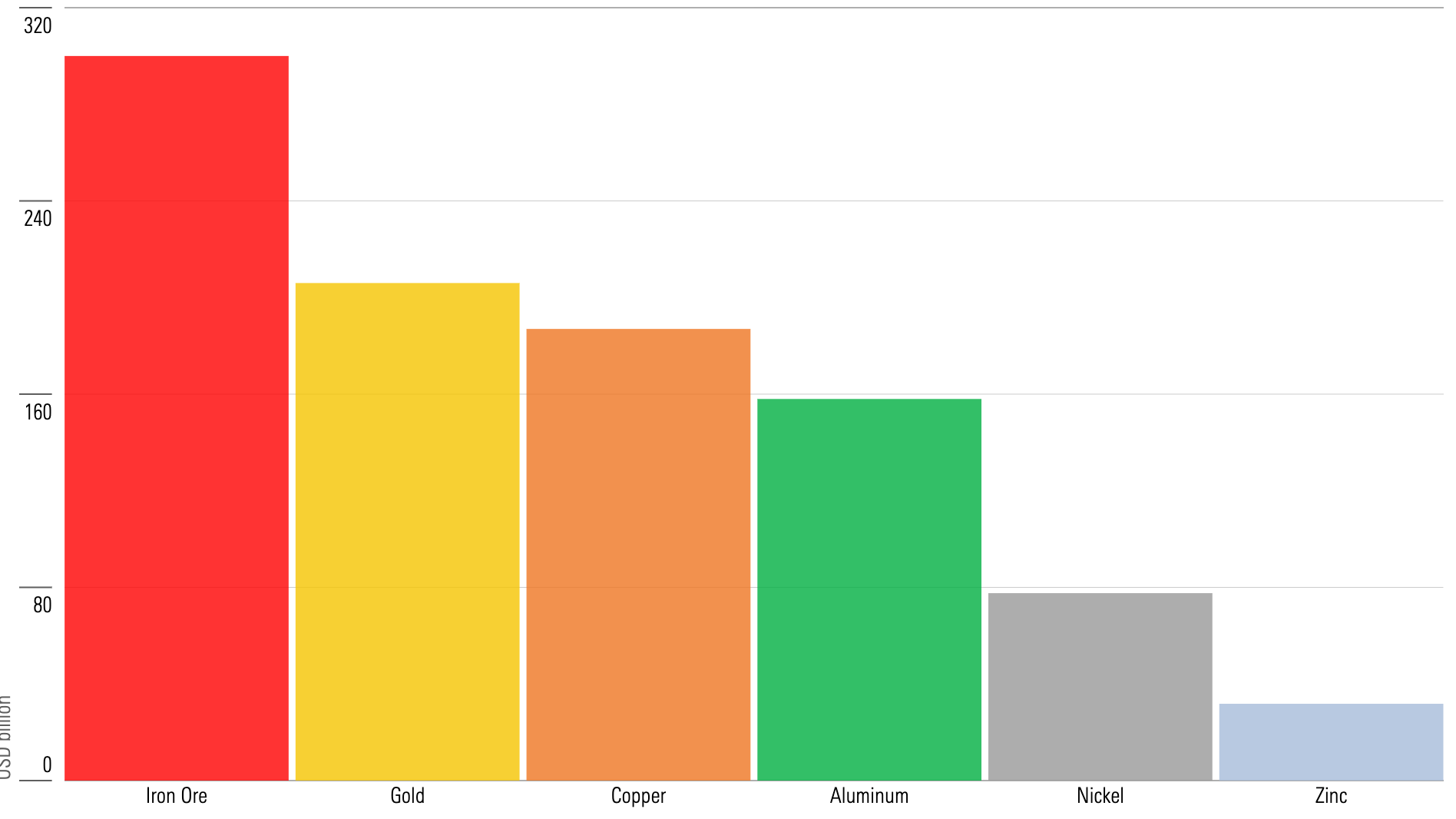

In this space, gold tends to capture the bulk of investor attention, but it’s actually the second-largest market by value in the mining industry: The largest is iron ore.

Three key themes driving the mining industry are:

- Spot prices are generally falling—though they’re still elevated overall.

- Unit costs for major miners are rising.

- Miners are tilting toward growth.

In our 2024 Mined Commodities Landscape Report, we outline our expectations for the industry through the lens of these themes and share a few investing opportunities.

3 Key Themes for the Mining Industry

Our outlook for the mining industry is centered on three key themes:

- Spot prices are generally falling—though they remain elevated overall. Demand growth from China has been the main driver of rising commodities prices in the past two decades. More recently, though, most commodities prices have fallen from highs set with Russia’s invasion of Ukraine, the subsequent sanctions on Russia, and the rerouting of supply chains. Prices, nevertheless, are generally elevated versus the 20-year average, as well as relative to cost support.

- Unit costs for major miners are rising. Costs tend to loosely track commodities price changes, albeit with a lag. Unit costs have risen in recent years, driven by rising commodities prices and cost inflation. They generally fell around the mid-2010s in response to falling prices and weak China demand but rose again as China stimulated investment and commodities demand. Longer term, commodities prices should trade close to the marginal cost of production, which is generally around the 90th percentile of the industry cost curve.

- Miners are tilting toward growth. Mines are depleting assets, so reserves need constant replenishment, either via exploration or mergers and acquisitions. Spending on exploration and M&A tends to be correlated with commodities prices. After many years of focusing on returning excess cash to shareholders—with gold miners being the notable exception by instead focusing on significant M&A—elevated commodities prices are now encouraging miners to tilt toward growth, particularly in energy transition commodities.

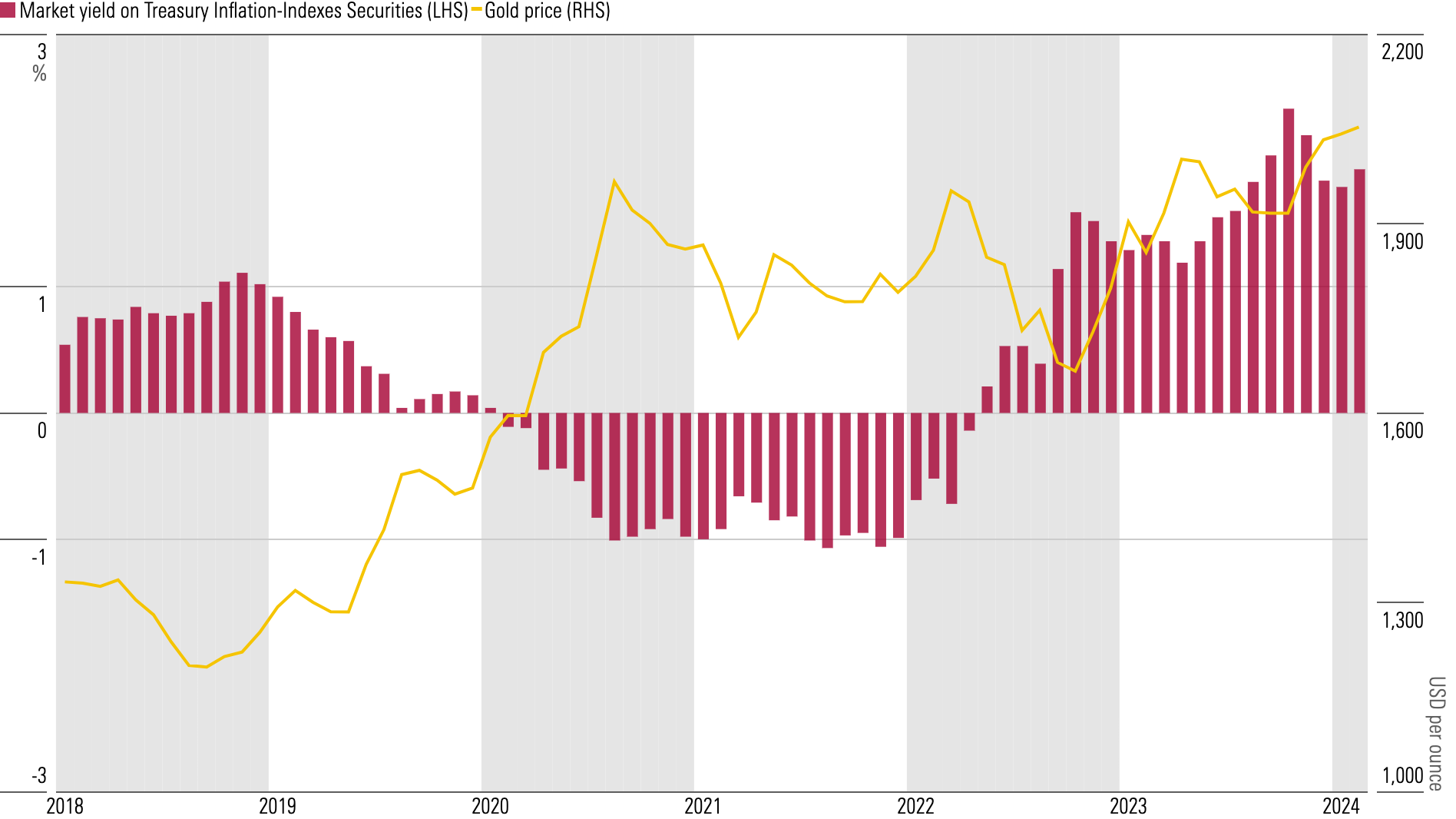

Gold Likely to Benefit From Falling Interest Rates

Gold prices tend to be negatively correlated to real interest rates. The lack of cash flow from gold increases the opportunity cost to hold it as rates rise and vice versa, which means expectations of falling real interest rates are boosting gold prices.

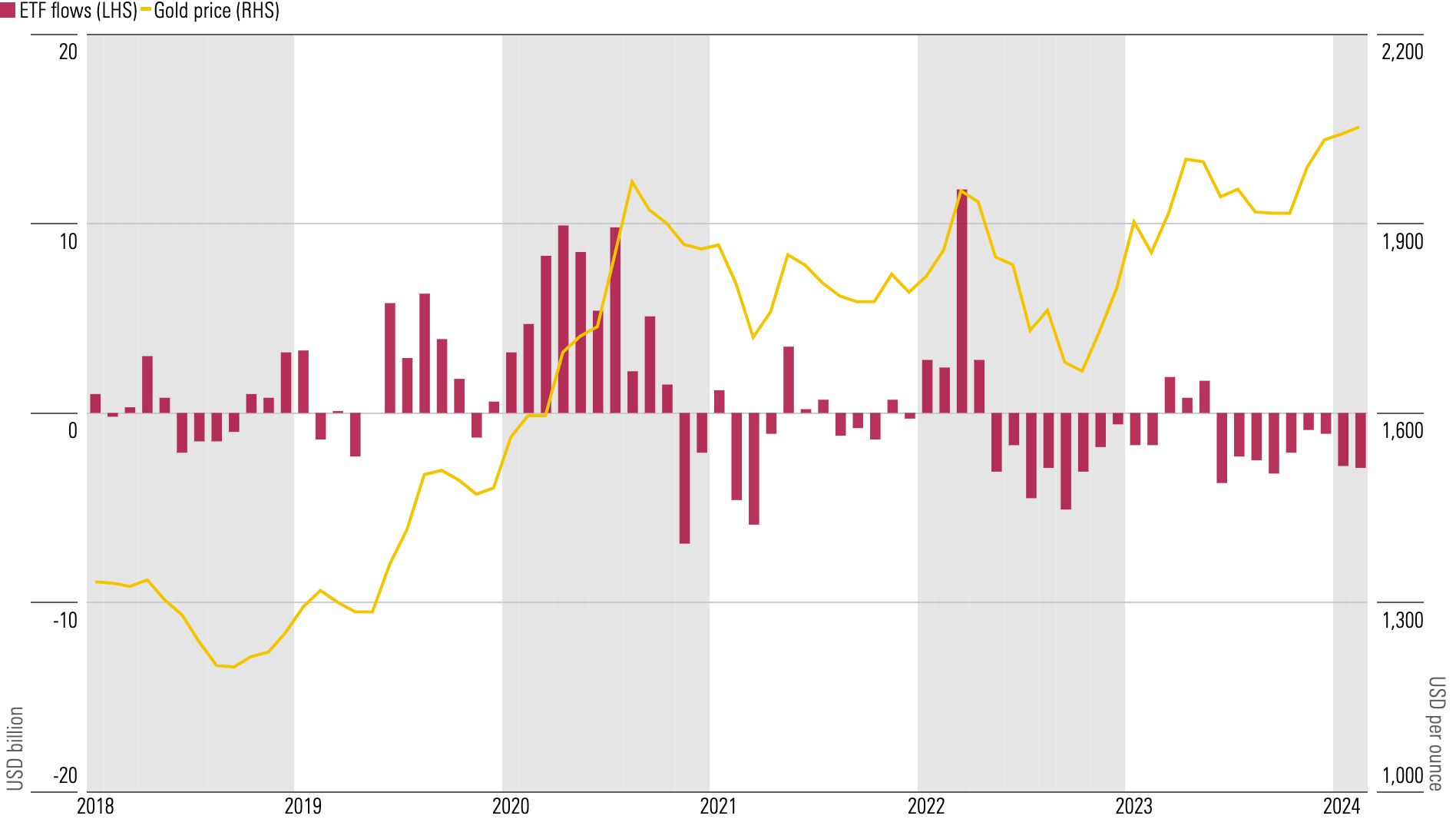

While jewelry is the biggest source of demand, exchange-traded funds tend to be marginal buyers of gold, responding to movements in gold prices. Rising gold prices suggest ETF flows could turn positive, further supporting gold prices.

One Mining Stock With a Wide Moat

Most of the mining companies on our coverage list have large market capitalizations, operate numerous mines, and are exposed to multiple commodities. Moats are rare, but with a Morningstar Economic Moat Rating of wide, Deterra Royalties is an exception.

Deterra Royalties DRR

- Primary Commodity: Iron Ore

- Morningstar Rating: 3 stars

- Morningstar Uncertainty Rating: Medium

- Fair Value Estimate (as of March 26, 2024): AUD 4.40

Deterra Royalties has earned its wide moat through its royalty on BHP’s Mining Area C, or MAC, iron ore operations. This rare asset is based on both cost advantage and intangible assets.

The intangible assets relate to the MAC royalty agreement among BHP BHP, BHP’s minority partners, and Deterra. The agreement sets out terms for royalty payments for iron ore produced from the MAC royalty area and additional payments for increasing mine capacity, and it defines the royalty area itself.

The cost advantage stems from both the low cost of acquiring the MAC royalty area and the low-cost iron ore production that underpins the royalty. The North and South Flank mines are expected to be close to the bottom quartile of the global cost curve at full capacity. High-quality resources are sufficient to underpin at least 30 years of life at North Flank and 25 years at South Flank, with additional development options nearby.

We think production is highly likely to continue even if iron ore prices crater, given the low-cost nature of MAC. This underpins the value of the intangible assets. The royalty is based on revenue rather than profits, and so isn’t directly affected by the margins BHP earns from MAC. If anything, the MAC royalty would likely benefit from inflation, assuming it ultimately steepens the cost curve and supports higher prices. Deterra has no operating costs and no capital costs but owns royalty rights on current and future developments in the royalty area. BHP is the primary counterparty and is in strong financial shape.

4 Undervalued Stocks in the Mining Industry

These companies don’t feature moats, but we still think they are materially undervalued.

This article was compiled by Emelia Fredlick.

Source link